Have you ever wondered about seller financing? As an investor, I'm sure you're aware of how advantageous seller financing can be for a buyer. However few buyers realize that sellers can benefit as well. This article will help clear up any confusion and explain the ins and outs of seller financing.

Concept Explained

The IRS defines an installment sale (owner/seller financing) as “a sale of property where you receive at least one payment after the tax year of sale.” For real estate, this means that the seller becomes the one holding the mortgage (instead of the bank) and the buyer makes agreed upon payments to the seller. Everything else remains the same from a contract stand point.

Applicability to Real Estate Investors

If you are the buyer, it is likely that the seller isn’t aware or hasn’t even explored the option of seller financing. If you are the seller, you should be aware of the below information to see if seller financing aligns with your overall financial plan.

The key tax benefits for the seller are:

The amount of depreciation recapture must be recaptured in the year of sale (therefore, the seller must set aside monies for this). Depreciation recapture is taxed at ordinary income rates, up to 25% for federal taxes. Additional taxes will be incurred if the state has income tax. Note that this would be paid anyway if the seller didn’t opt to do a 1031 exchange. However, the seller will now have the ability to spread out the taxes on the gain from the sale (excluding depreciation recapture) over a longer period of time.

Ability to collect predictable monthly payments from the buyer. The interest portion paid will be taxed as interest and a portion of the principal paid each year will be taxed as a capital gain.

Less taxable income year after year over the duration of the loan despite getting the same monthly payment. This is because there is lower interest being paid (given the nature of amortization tables).

The key tax benefits for the buyer are:

Even though little money is put down, just like all other depreciable real estate, the buyer gets the full benefits of depreciation. In other words, even though the buyer may be putting in perhaps 5-10%, he/she still gets all of the depreciation benefits of real estate. Nothing changes in the installment scenario.

The buyer still receives the same interest deductions for their monthly payments.

Detailed Example

The below example focuses exclusively on the seller and goes into more detail than you probably need to share in an initial conversation around seller financing. However, understanding this breakdown is imperative to moving the seller financing conversation along. The example uses round numbers for ease, and assumes that both the close date is and first payment date is 1/1/21.

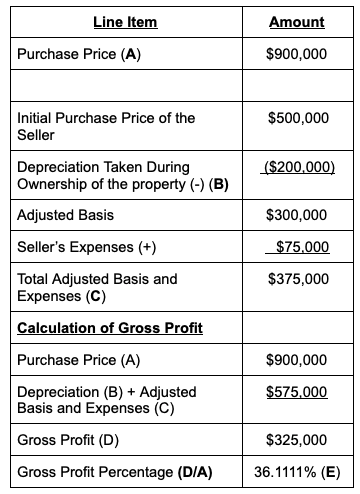

Assume the building is currently being sold for $900,000. The initial purchase price by the seller was $500,000 and the depreciation taken during ownership was $200,000. The seller is left with an adjusted basis of $300,000. From there, the seller gets to add selling expenses of $75,000 to their adjusted basis. Total adjusted basis and expenses are now $375,000.

Now, the seller must calculate the gross profit by taking the purchase price less depreciation (since this will be recaptured at ordinary rates up to 25%) less the adjusted basis and selling expenses. The seller is left with a gross profit of $325,000 and therefore a gross profit percentage of 36.1111%. Results are summarized below. Please note that this gross profit percentage will apply for the year of sale and for all of the years after for seller financing.

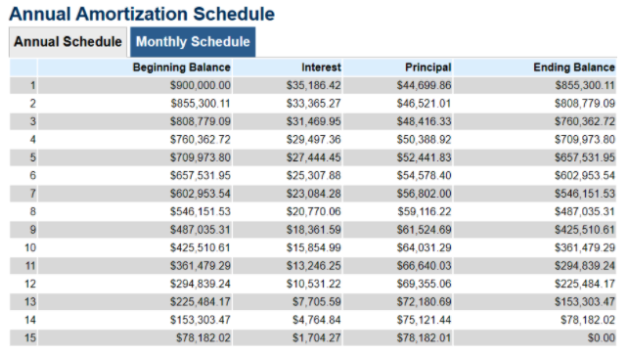

The seller has generously decided to take back the entire purchase price (fortunate for the buyer) over a 15 year term at a 4% interest rate. The amortization table below is a reflection of this.

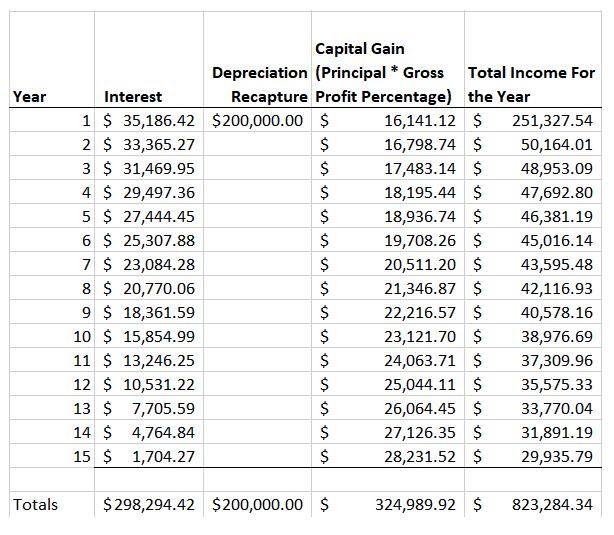

The interest above will be taxed as interest for the seller and a deduction for the buyer. Further, a portion of the principal (equal to the gross profit percentage of 36.1111%) will be considered a capital gain. For the calculations, see the below chart. You will note that the seller will have less taxable income as the years go (a key benefit to the seller listed above).

Conclusion

Seller financing has significant benefits for the buyer and seller when done right. The seller gets to stretch out the tax bill over the length of the note and receive steady monthly payments. The buyer is able to get into a property without bank financing and potentially get in with less money down then they otherwise would have with bank financing. There are many tax considerations that must be communicated to the seller when going this route as it can be quite complicated. My hope is that the example above will help serve as a guide for explaining seller financing to a potential seller.

If you have questions on your real estate tax strategy, you can reach me (Aaron Zimmerman) at aaronz@thethinkers.com.

Additional Resources:

Amortization Calculator Used For Example

Tax Forms Needed for Seller Financing:

Looking for a Property Manager? Schedule a call today or visit our website for more information.

Get your FREE copy of: Top 10 Mistakes Investors Make When Working With Lenders

Extra Hacks & Tricks from Expert Investors? Join Our Facebook Group!

Missed something? Subscribe to our Youtube Channel!

LISTEN to our Podcast on iTunes | Spotify | Stitcher | TuneIn Radio

Need A Responsive Property Manager? We’ve got you covered!

![]()

![]()