When you close on a property, at the closing you are going to receive the Closing Disclosure. This will show you, amongst other things, your principal and interest, mortgage insurance, escrow amounts, and cash to close. However, in terms of accounting, there is so much more information that will become valuable as detailed below. In this article, we will go section by section to see what’s important to keep track of and what’s not.

Definitions

Loan costs- all costs necessary to obtain the loan. These costs will ultimately be amortized over the life of the loan.

Initial Cost Basis - all costs associated with the purchase of the property. These costs will be depreciated over the life of the property.

Escrow - amounts placed in special holding accounts for your property tax payments and homeowner’s insurance premiums. Amounts placed here are non deductible.

Expenses - These are not associated with any of the above. These costs are customary and necessary within the course of your real estate business. In real estate, expenses become expenses when they have been incurred.

Section By Section Walkthrough

Loan Costs

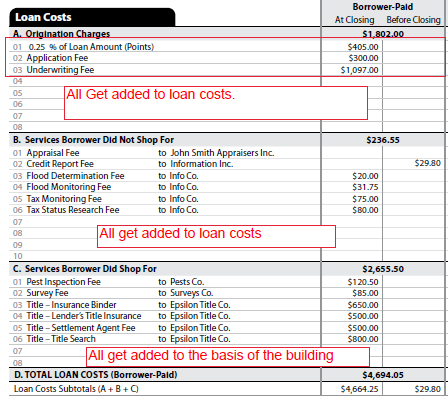

Loan costs are the first section of the closing disclosure. Below is an example.

In the first section, “Origination Charges”, you will typically see the charges that the lender will provide to you. All of these costs will be loan costs as they are necessary to obtain the loan.

In section B, services borrower did not shop for, all of the costs above will be loan costs as these were paid to obtain the loan. However, one common item that isn’t listed is the mortgage insurance premium, which is 1.75% of the loan amount. This is arguably the biggest planning opportunity. With the mortgage insurance premium, you can either expense it all in year one or you could add it to the loan costs. You will want to discuss with your tax advisor what is best for you and your specific situation. For instance, if you plan on purchasing additional property, you may want to include it with loan costs as you will have fewer expenses and therefore more income to obtain additional loans.

In section C, “Services Borrower Did Shop For”, all of these costs get added to the basis of the building. Generally, this section includes title fees.

Other Costs

.png)

For Section E, these costs will be included in basis as these are necessary to purchase the property. You will most likely see a high transfer tax in Cook County on the buyer’s side (.8% of the purchase price), so be sure to not miss this.

For Section F, two of the items are expenses and two of the items are escrow items. The two expenses are: homeowner’s insurance premium and prepaid interest. The two escrow items are mortgage insurance premium (which would be for placing funds into escrow) and property taxes. Sometimes there are no amounts in this section, but instead are listed in Section G.

For Section G, these would be comparable to Section F and only relate to escrow. Any aggregate adjustment, you can simply ignore as this is likely related to the escrow.

For Section H, generally these are all added to basis. Other items not included here would be fees paid to your real estate attorney. This would also be added to basis.

Summaries of Transactions

.png)

For Section K, the biggest item to note here is the sale price of the property. This will be added to your initial basis. The closing costs have already been accounted for. The HOA dues would not be accounted for here.

For section L, you will deduct the seller’s credits from the basis. You would also deduct the rebate from the title company above as well. For the property tax credit, please see my previous article for how to handle this.

Putting It All Together

After completing the above, you will divide into three categories: basis in property, loan costs, and expenses. The below summarizes all of the sections above. The first two columns are something that you would want to provide to your accountant. The third section, expenses, would be added to your monthly bookkeeping software/tracking system. From there, you would also need to allocate between building (depreciable) and land (non depreciable). See my article here for how to do that.

.png)

Conclusion

Figuring out the basis in your property does not have to be difficult. With the template above, you will be able to figure out your basis relatively quickly. Another added benefit of doing this is that you will be able to figure out your depreciation deduction. This should help you have a clearer picture of your taxes when you ultimately file your return.

If you have questions on your real estate tax strategy, you can reach me (Aaron Zimmerman) at aaronz@thethinkers.com.

Looking for a Property Manager? Schedule a call today or visit our website for more information.

Get your FREE copy of: Top 10 Mistakes Investors Make When Working With Lenders

Extra Hacks & Tricks from Expert Investors? Join Our Facebook Group!

Missed something? Subscribe to our Youtube Channel!

LISTEN to our Podcast on iTunes | Spotify | Stitcher | TuneIn Radio

Need A Responsive Property Manager? We’ve got you covered!