LLCs are frequently talked about within real estate circles. Most people are aware of the asset protection benefits that LLCs provide. However, the important tax implications are not as often highlighted. In this article, I will be discussing key terms, what you need to know about LLCs, and how this applies to your real estate business.

Definitions

A multi-member LLC means having more than one member in the LLC (Limited Liability Company). For this entity, you will typically file a partnership return (form 1065). Each partner receives what’s called a “K1” which shows your distributive share of income/loss and distributions from the partnership.

Basis is the amount of capital investment in the property for tax purposes.

Qualified nonrecourse financing - Includes financing for which no one is liable for repayment, and that is borrowed for use in an activity of holding real property. It is loaned or guaranteed by a federal, state, or local government or borrowed from a qualified person.

Recourse - A loan in which you are personally liable for.

Qualified Business Income Deduction - defined here

Distributions - Payment of cash or property to the entity’s members.

What You Need to Know About Multi-Member LLCs

There are five separate pieces of an LLC that are important to note. First, who is active and who is passive? How do you determine this? Second, I will discuss how the basis is calculated and share a few examples. Third, how do you know if you can take losses? We will then touch briefly on the taxation and the qualified business income deduction.

Active vs Passive

There are seven key tests that determine whether an investor is active or passive. This article nicely summarizes the tests to determine whether you’re active or passive within the LLC. To be active, you only need to pass one of them.

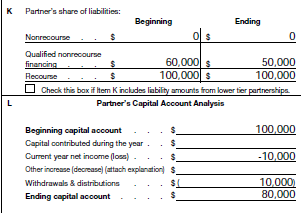

Basis

It is important to know your basis for tax purposes as this could impact the deductibility of your losses and treatment of your distributions. Your basis is a formula as follows:

Qualified nonrecourse financing + recourse +/- Ending capital account

The reason this is important is because you cannot take losses that exceed your basis. Further, you can not take distributions that exceed your basis (without being taxed). Typically, you will want to make sure, at the partnership level, that distributions are appropriately handled so the members do not have any tax surprises. Should that not be the case and distributions do exceed your basis, this will end up being reported as a capital gain.

Example 1:

An investor starts the year off with $100,000 in their capital account. The LLC itself owns a 10 unit apartment building. Further, they are also on the hook for $100,000 as they lent the LLC money (recourse) and additional qualified non-recourse financing of $60,000 for the loan on the property. In total, their beginning basis is $260,000 ($100,000 + $100,000 + $60,000). During the year, this member’s share of loss was $10,000, and due to the strong cash flow of the building, this member was able to take $10,000 out in distributions. In total, their capital account decreased to $80,000. The LLC also paid down debt of $10,000. As such, their ending basis is $230,000 ($50,000 + 80,000 + 100,000).

Example 2:

This is year six of the partnership. Much of the depreciation on the 10 unit apartment building owned by the LLC has been taken. Further, many years of distributions have been taken leading to a negative beginning capital account balance of $75,000. During the year, the LLC decided to refinance due to strong appreciation in the market and their ability to operate on their business plan. As such, they obtained a loan for 150% more than their beginning loan balance. Due to this refinance, the LLC distributed a portion of that to their member’s. For this specific member, $25,000 was distributed (thus lowering their capital account). The LLC also lost $5,000 during the year. At year end, the basis per member was still positive $70,000 ($125,000 + $50,000 - $105,000).

_1.png)

Taking Losses

Taking losses depends on whether you are active or passive. If you are active, you can offset your active income with these losses up to your basis. If you are passive, you can only offset passive losses with passive income from other sources. If there is no passive income, the losses get carried forward from year to year until the property is disposed of.

Example 1: Active Investor

Using example #1 above, let’s assume the active investor lost $10,000 during the year. They would be able to deduct that loss against their income due to the basis being positive. No matter the income, you can deduct your active losses against active income.

Example 2: Passive investor #1 - Carryforward losses

Using example #1 above, let’s instead assume the investor is passive. The loss is still $10,000. However, since they are passive, they can only offset their losses with other passive income. The investor has no other passive income. As such, the $10,000 is carried forward to next year.

Example 3: Passive investor #2 - Offsetting losses with income

Still using example #1 above, the investor has a $10,000 passive loss. This investor is also passive in a number of other partnerships that have generated $11,000 in passive income. Since the losses and the income are both passive, these offset and are netted together. Instead of paying taxes on the $11,000, taxes are paid on only $1,000 for this year.

Taxation

Multi-member LLCs can be taxed as S-Corporations or C Corporations (provided you request this from the IRS). This is outside the scope of this article but is important to note.

What is important to note is that the partner will typically receive a K-1 assuming they are filing as a partnership or S Corporation. This must go on your Schedule E of your individual tax return. You will know if this is done right if you see this appear on page 2 of your Schedule E.

Qualified Business Income Deduction

Partnerships are eligible for the qualified business income deduction as well provided they invest in qualifying real estate and generate positive income. The deduction is limited to the greater of (1) 2.5% of unadjusted basis of the property plus 25% of W-2 wages or (2) 50% of W-2 wages paid. Typically in real estate, you will be limited by the first one. You would want to talk to your accountant to figure exactly how much impact, if any, this will have for your specific situation.

Wrapping It Up

The two biggest items of the above that you should truly care about for your real estate business are the ability to take losses and basis. You should be able to explain this to your fellow members (or have your accountant do it). You will want to make sure the members know in advance if they will be able to deduct losses (if there are any) and what impact, if any, distributions will have on their taxes. In fact, if it’s easier, refer them to this article!

If you have questions on your real estate tax strategy, you can reach me (Aaron Zimmerman) at aaronz@thethinkers.com.

Looking for a Property Manager? Schedule a call today or visit our website for more information.

Get your FREE copy of: Top 10 Mistakes Investors Make When Working With Lenders

Extra Hacks & Tricks from Expert Investors? Join Our Facebook Group!

Missed something? Subscribe to our Youtube Channel!

LISTEN to our Podcast on iTunes | Spotify | Stitcher | TuneIn Radio

Need A Responsive Property Manager? We’ve got you covered!